Concrete

Pyroprocessing: The Heart of the Matter

Design, technology, innovation and costs are the determining factors for the future of pyroprocessing in cement production.

At the heart of the Portland Cement manufacturing process is the pyroprocessing system. This system transforms the raw mix into clinkers, which are grey, glass-hard, spherically shaped nodules that range from 0.32 to 5.1 (cm) or (0.125 to 2.0 inches [in.]) in diametre. The chemical reactions and physical processes that constitute the transformation are quite complex, but they can be viewed conceptually as sequential events starting with:

- Calcination of the calcium carbonate (CaCO3) to calcium oxide (CaO);

- Reaction of CaO with silica to form dicalcium silicate;

- Reaction of CaO with the aluminum and iron-bearing constituents to form the liquid phase;

- Formation of the clinker nodules;

- Evaporation of volatile constituents (e. g. sodium, potassium, chlorides and sulphates);

- Reaction of excess CaO with dicalcium silicate to form tricalcium silicate.

There are three distinct temperature phases as well in pyroprocessing:

Dehydration, as the material temperature increases from 100°C to approximately 430°C (800°F) to form oxides of silicon, aluminum, and iron; Calcination, during which carbon dioxide (CO2) is evolved, between 900°C (1650°F) and 982°C (1800°F), to form CaO; and Reaction of the oxides in the burning zone of the rotary kiln, to form cement clinker at temperatures of approximately 1510°C (2750°F).

These processes in its entirety transforms the limestone molecular structure into clinker and the process involves high temperature heating of the raw mix needing energy (3250 megajoules per tonne) and the emissions include a slew of gases, mostly CO2 and NOx, that is 800 kg per tonne of cement produced; thus, the focus has been to reduce carbon intensity, increase usage of alternate fuels stemming from wastes and improve efficiency simultaneously. The direction in which technology has evolved would be the focus of this short note.

Preheather Process

Dry process pyroprocessing systems have been improved in thermal efficiency and productive capacity through the addition of one or more cyclone-type preheater vessels in the gas stream exiting the rotary kiln. This system is called the preheater process. The vessels are arranged vertically, in series, and are supported by a structure known as the preheater tower. Hot exhaust gases from the rotary kiln pass counter currently through the downward-moving raw materials in the preheater vessels. Compared to the simple rotary kiln, the heat transfer rate is significantly increased, the degree of heat utilisation is greater, and the process time is markedly reduced by the intimate contact of the solid particles with the hot gases. The improved heat transfer allows the length of the rotary kiln to be reduced. The hot gases from the preheater tower are often used as a source of heat for drying raw materials in the raw mill. Because the catch from the mechanical collectors, fabric filters, and/or electrostatic precipitators (ESP) that follow the raw mill is returned to the process, these devices are considered to be production machines as well as pollution control devices.

Additional thermal efficiencies and productivity gains have been achieved by diverting some fuel to a calciner vessel at the base of the preheater tower. This system is called the preheater/precalciner process. While a substantial amount of fuel is used in the precalciner, at least 40 per cent of the thermal energy is required in the rotary kiln. The amount of fuel that is introduced to the calciner is determined by the availability and source of the oxygen for combustion in the calciner. Calciner systems sometimes use lower-quality fuels (e. g. less-volatile matter) as a means of improving process economics.

Preheater and precalciner kiln systems often have an alkali bypass system between the feed end of the rotary kiln and the preheater tower to remove the undesirable volatile constituents. Otherwise, the volatile constituents condense in the preheater tower and subsequently recirculate to the kiln. Build-up of these condensed materials can restrict process and gas flows. The alkali content of Portland cement is often limited by product specifications because excessive alkali metals (i. e. sodium and potassium) can cause deleterious reactions in concrete. In a bypass system, a portion of the kiln exit gas stream is withdrawn and quickly cooled by air or water to condense the volatile constituents to fine particles. The solid particles, containing the undesirable volatile constituents, are removed from the

gas stream and thus the process by fabric filters and ESPs.

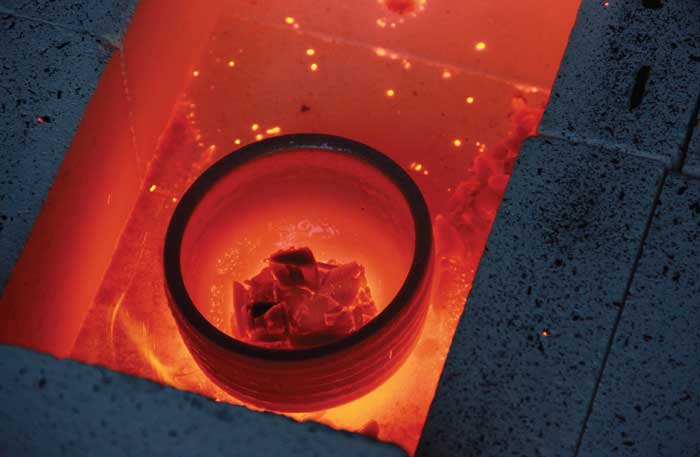

Clinker Cooler

The last component of the pyroprocessing system is the clinker cooler. This process recoups up to 30 per cent of the heat input to the kiln system, locks in desirable product qualities by freezing mineralogy, and makes it possible to handle the cooled clinker with conventional conveying equipment. The more common types of clinker coolers are (1) reciprocating grate, (2) planetary, and (3) rotary. In these coolers, the clinker is cooled from about 1100°C to 93°C (2000°F to 200°F) by ambient air that passes through the clinker and into the rotary kiln for use as combustion air. However, in the reciprocating grate cooler, lower clinker discharge temperatures are achieved by passing an additional quantity of air through the clinker. Because this additional air cannot be utilised in the kiln for efficient combustion, it is vented to the atmosphere, used for drying coal or raw materials, or used as a combustion air source for the pre-calciner.

satisfy set emission limits.

The direction and focus so far in pyroprocessing, including the cooler, has been to increase thermal efficiency, followed by emission control to achieve the desired level as stipulated by regulatory authorities. On this second aspect optimised kiln burners, staged combustion calciners, and SNCR- as well as SCR-systems are the prevalent solutions available to satisfy set emission limits. On the former mostly technologies on offer must optimise alternate fuels, raw mill mix feed and the efficiency factors as a combined objective function, where cost economics have always played the most dominant role.

Cost economics starts with the dynamic prices of all fuel types and their landed cost converted to Rs/Kcal, which creates some parity but the combination in which this can be optimised has many other dynamic factors that include chemistry and thermal dynamics together with the quality attributes.

Most cement companies have remained straddled between the cost economics and the emission goals and until recently had remained hinged to the goals of cost economics that did not preclude the externalities involved or the abatement costs. The procurement cost of all types of fuel for the pyroprocessing also did not factor in the internal price of carbon.

Thus, pyroprocessing economics could be changing very dramatically once the future pricing dynamics start to include all of these costs; the design of the future pyroprocessing system could be ordained on a very different objective function that must optimise a number of factors, not necessarily the ones that are on the top of the agenda.

Procyon Mukherjee

Concrete

Shree Digvijay Cement Reports Annual And Quarterly Results

Annual revenue rises as EBITDA expands sequentially

Concrete

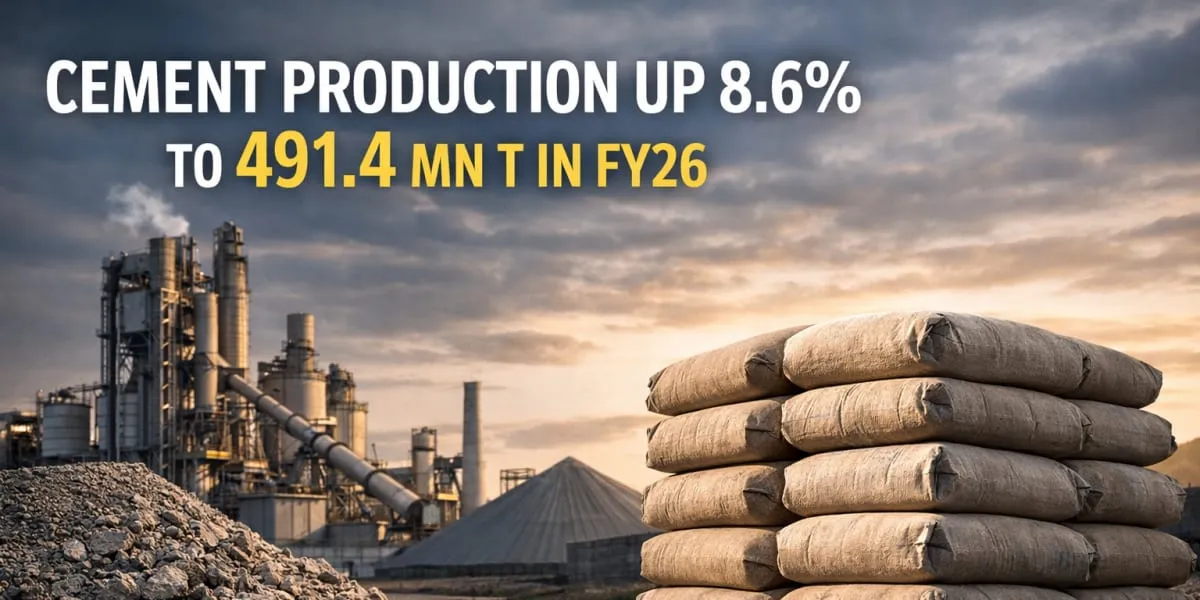

Cement Production Up Eight Point Six Per Cent To 491.4 mn t In FY26

Icra Sees Seven To Eight Per Cent Growth In FY27

Concrete

UltraTech Cement FY26 PAT Crosses Rs 80 bn

Company reports record sales, profit and 200 MTPA capacity milestone

Shree Digvijay Cement Reports Annual And Quarterly Results

Cement Production Up Eight Point Six Per Cent To 491.4 mn t In FY26

UltraTech Cement FY26 PAT Crosses Rs 80 bn

Towards Mega Batching

Andhra Offers Discom Licences To Private Firms Outside Power Sector

Shree Digvijay Cement Reports Annual And Quarterly Results

Cement Production Up Eight Point Six Per Cent To 491.4 mn t In FY26

UltraTech Cement FY26 PAT Crosses Rs 80 bn

Towards Mega Batching