Concrete

Global Emission Pathways: Need for Urgent Action

The Indian cement industry knows the premise it stands on, in terms of carbon emissions.

The Indian cement industry knows the premise it stands on, in terms of carbon emissions. What remains is an accelerated effort in tackling the imminent issue of climate change and making good all its commitments for net zero. The Race-to-Zero is not just a race against carbon emission, it is one against time.

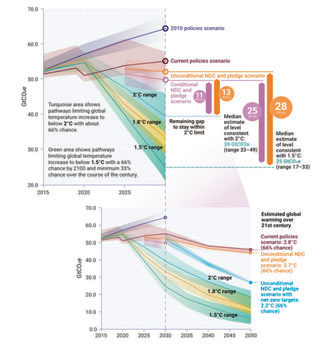

The presentation below is taken from the Emissions Gap Report published by the partnership of UN Environmental Program (UNEP) and DTU late in October, just preceding the Climate Summit at Glasgow. The data is revealing, the message is loud and clear that the current pledges and actions included do not bode well for the trajectory of emissions moving forward into 2030 or beyond. There is a lot more that needs to be done.

The summary of the report, given as its foreword, states, “To get on track to limit global warming to 1.5°C, the world needs to take an additional

28 gigatonnes of carbon dioxide equivalent (GtCO2e) off annual emissions by 2030, over and above what is promised in updated unconditional NDCs.” NDC or the Nationally Determined Contribution is the guiding light for tracking initiatives against reduction in emissions as declared by nations.

What does the report card say so far on what we have done from 2010 to now; the current actions put in place will reduce 11 GtCO2e in 2030, now that is not a small number, had these actions not been put on ground, so much progress would not have happened.

But the reality is very different, the world still emits close to 50 GtCO2e per year and that means the stock of emissions is rising by the day and much more needs to be done till we reach a state of no further rise in stock. That is where the pledges of net zero come in, when from corporate to the common man to the communities and government, who take decisions every day, it will come as the overriding priority to act.

Realistic goals

Let us dig into some details of where we are headed, given this conundrum, despite the discussions and agreements so far, the Glasgow talks included. Let us start with some bad news that the euphoria about the 5.4 per cent drop in emissions in 2020 was short lived, thanks to the pandemic, as it is now predicted that the emissions will bounce back to a rise of 4.8 per cent over 2020 in 2021. The peculiar case is that despite a drop in CO2 emissions the concentration of CO2 in the atmosphere grew by 2.3 parts per million, which effectively means that the atmosphere would never even feel any change.

The second area to look at would be the mitigation pledges and where they fall short of the target. The way to look at these pledges is to look at the NDCs. Just under half (49 per cent ) of the new or updated NDCs submitted (from countries accounting for 32 per cent of global emissions) result in lower 2030 emissions than the previous NDC. Around

18 per cent of the NDCs (from countries accounting for 13 per cent of global emissions) will not reduce 2030 emissions relative to the previous NDC. The remaining 33 per cent of NDCs (from countries accounting for 7 per cent of global emissions) contain insufficient detail to assess their impact on emissions relative to the previous NDC.

As a group, G20 members are not on track to achieve either their original or new 2030 pledges. Ten G20 members are on track to achieve their previous NDCs, while seven are off track. The US EU27, the UK and Canada are the top countries that have shown a higher change in emission reduction.

Only 10 G20 members (Argentina, China, EU27, India, Japan, the Russian Federation, Saudi Arabia, South Africa, Turkey and the UK) are likely to achieve their original unconditional NDC targets under current policies. Among them, three members (India, the Russian Federation and Turkey) are projected to reduce their emissions to levels at least 15 per cent lower than their previous unconditional NDC emissions target levels under current policies.

A promising development is the announcement of long-term net zero emissions pledges by 50 parties, covering more than half of global emissions. However, these pledges show large ambiguities. Few of the G20 members’ NDC targets put emissions on a clear path towards net zero pledges. There is an urgent need to back these pledges up with near-term targets and actions that give confidence that net zero emissions can ultimately be achieved and the remaining carbon budget kept.

Twelve G20 members covering just over half of global domestic GHG emissions have currently pledged a net zero target, of which six are in law, two are in policy documents and four are government announcements. All are for the year 2050, with the exception of China’s 2060 target and Germany’s target for 2045. The remaining eight G20 members have so far not set net zero targets, but three of them have communicated long-term low GHG emission development strategies to the UNFCCC (Indonesia, Mexico and South Africa).

Only Canada, the European Union, France, Germany and the Republic of Korea have published their plans at the time of completing this report, and only these countries plus the United Kingdom have accountable processes for reviewing their targets.

The emissions gap remains large; compared to previous unconditional NDCs, the new pledges for 2030 reduce projected 2030 emissions by only

7.5 per cent , whereas 30 per cent is needed for 2°C and 55 per cent is needed for 1.5°C.

Two very significant findings are:

1. Global warming at the end of the century is estimated at 2.7°C if all unconditional 2030 pledges are fully implemented and 2.6°C if all conditional pledges are also implemented. If the net zero emissions pledges are additionally fully implemented, this estimate is lowered to around 2.2°C.

2. The opportunity to use COVID-19 fiscal rescue and recovery spending to stimulate the economy while fostering a low-carbon transformation has been missed in most countries so far. Poor and vulnerable countries are being left behind.

This leaves us with two decisive areas of focus:

A. Reduction of methane emissions from the fossil fuel, waste and agriculture sectors can contribute significantly to closing the emissions gap and reduce warming in the short term.

B. Carbon markets can deliver real emissions abatement and drive ambition, but only when rules are clearly defined, designed to ensure that transactions reflect actual reductions in emissions, and supported by arrangements to track progress and provide transparency.

The case for negotiations is well understood as with nations like India and China, who have a lot at stake on the Coal related tapering off to be done over the next decades and this is not an easy task. The next area is to focus on the investment vehicles to focus on decarbonising several of the fossil fuel guzzling industries, where the net zero pledges must have a way of formal review. This is where the world’s attention must be focused on.

Procyon Mukherjee

Concrete

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Line-2 expansion to make Kadapa a major cement hub

Concrete

Cement Prices to Stay Flat in Q2 FY27 as Costs Squeeze Margins

HDFC Securities warns monsoon slowdown and higher fuel costs

Concrete

Dalmia Bharat Begins Rs 31 Bn Green Cement Unit in Kadapa

New Andhra Pradesh plant to add 9.6 MTPA cement capacity by FY28

Fornnax Names Lukas Baur as Authorised Service Partner to Bolster EU Operations

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Cement Prices to Stay Flat in Q2 FY27 as Costs Squeeze Margins

Dalmia Bharat Begins Rs 31 Bn Green Cement Unit in Kadapa

Nuvoco Inaugurates Limla Cement Plant in Surat

Fornnax Names Lukas Baur as Authorised Service Partner to Bolster EU Operations

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Cement Prices to Stay Flat in Q2 FY27 as Costs Squeeze Margins

Dalmia Bharat Begins Rs 31 Bn Green Cement Unit in Kadapa

Nuvoco Inaugurates Limla Cement Plant in Surat

-

Concrete4 weeks ago

Concrete4 weeks agoACC To Expand Cement Capacity Amid Strong Infrastructure Demand

-

Concrete4 weeks ago

Concrete4 weeks agoIndian Railways Plans Green Fly Ash Transport Network

-

Concrete4 weeks ago

Concrete4 weeks agoStar Cement Named Preferred Bidder For Boro Lakhindong Block

-

Concrete4 weeks ago

Concrete4 weeks agoKERC Proposal To Cut Rooftop Solar Export Tariff Raises Concern