Concrete

Blended Cement Grinding: Energy Intake and Fineness

ICR delves into the nuances of the grinding processes to understand its impact on energy consumption, quality of output and technology as well as the methodology of producing green cement.

The early adopters of the cement grinding process involved extracted clinker from the clinker tank and transported it to the cement mill hopper by belt conveyors, where a measured quantity of clinker and gypsum was fed into a closed-circuit ball mill and OPC was produced through inter-grinding and blending of 95 per cent clinker with 5 per cent gypsum.

The initial problem was coarseness, as 20 per cent over 100-micron diameter was part of the ground cement. Today with advancement of technology the fineness has been improved (3200 gm/square cm) by adopting specialised steel in the grinding equipment, together with use of grinding media, steel balls where material fed through the mill is crushed by impact and ground by attrition between the balls. The grinding media are usually made of high-chromium steel. Fineness is a controlled parameter for cement to ensure better hydration and strength development. Ground cement is then stored in a water-proof concrete silo for packing.

Making Cement Green

The rise of blended cement, starting from use of fly ash (30 per cent to 35 per cent) in PCC and blast furnace slag (65 per cent to 70 per cent) in slag-based cement, as an additive with clinker, together with 5 per cent gypsum, made the introduction of green cement as a better environment friendly product. The use of fly ash or blast furnace slag with clinker created avenues for commercial consumption of coal-fed pPower plant waste (fly ash) and steel blast furnace waste (slag) leading to the green cement that used 60 per cent of clinker in PCC and 35 per cent clinker in slag based cement.

This development has seen progressive increase of both fly ash and slag in the ground cement as well as in concrete, where fly ash or ground slag is added to OPC at the concreting stage. Such processes had enormous logistics challenges and in India the adoption of such a process during concreting is less prevalent.

Grinding a mixture of clinker with the fly ash or slag, together with gypsum has implications of cost stemming from use of electricity for grinding and landed cost of all inputs for the grinding process. Cement grinding is the single biggest consumer of electricity in the entire manufacturing process of cement, the rest is in the grinding of limestone in the crushers and in the fuel mills for grinding fuel used in the clinkerisation process. Finished grinding may consume 25-50 kWh/t cement, depending on the feed material grindability, additives used, plant design and especially the required cement fineness.

The grinding process absorbs more energy due to the losses attributable to heat generated during grinding, friction wear, sound noise and vibration. Less than 20 per cent of energy absorbed is reckoned to be converted to useful grinding: the bulk is lost as heat, noise, equipment wear and vibration. For ball mills, only 3 to 6 per cent of absorbed energy is utilised in surface production, the heat generated can increase mill temperature to more than 120⁰ C and causes excessive gypsum dehydration and media coating, if mill ventilation is poor.

Understanding the Process

There are four types of grinding mills in use today are:

Ball Mill (BM): Predominant despite higher energy consumption partly because of historical reasons but partly also because it still offers considerable advantages over other mills, often operating with roller press for pre-grinding or in combined grinding.

Vertical Roller Mill (VRM): Gained popularity in the last decade due to lower energy consumption and higher capacity, with relatively few plants in service.

Roller Press (RP): A more recent choice especially after the advent of the V-separator and improved roller life, offers the lowest energy consumption but even few plants in service.

Horizontal Mill (HM): A very few in service and found mainly in companies related to the

mill developer.

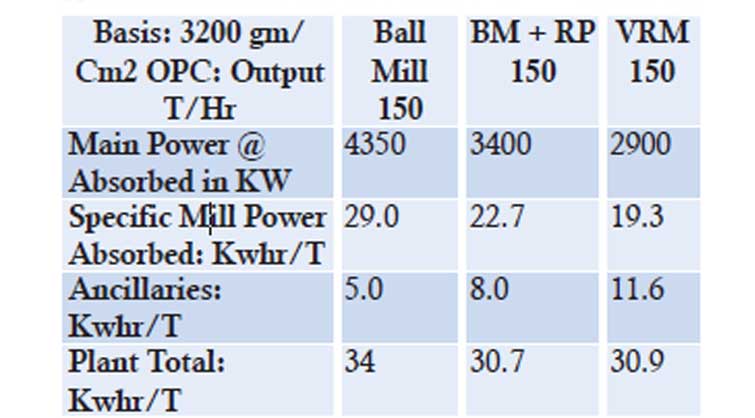

The chart below shows the relative power consumption for the different types of grinding process:

The implications of higher cost in installation, maintenance, operating cost, availability and quality of ground cement, makes the BM still the most common type of technology used, while VRM scores on electrical consumption.

The role of grinding media cannot be ignored in this entire process of grinding. The BM is a horizontal cylinder partly filled with steel balls (or occasionally other shapes) that rotates on its axis, imparting a tumbling and cascading action to the balls. Material fed through the mill is crushed by impact and ground by attrition between the balls. The grinding media are usually made of high-chromium steel. The smaller grades are occasionally cylindrical (‘pebs’) rather than spherical. There exists a speed of rotation (the ‘critical speed’) at which the contents of the mill would simply ride over the roof of the mill due to centrifugal action. The critical speed (rpm) is given by: nC = 42.29/√d, where d is the internal diameter in metres. A BM is normally operated at around 75 per cent of critical speed, so a mill with diameter 5 metres will turn at around 14 rpm.

The mill is usually divided into at least two chambers (although this depends upon feed input size – mills including a roller press are mostly single-chambered), allowing the use of different sizes of grinding media. Large balls are used at the inlet, to crush clinker nodules (which can be over 25 mm in diameter). Ball diameter here is in the range 60–80 mm. In a two-chamber mill, the media in the second chamber are typically in the range 15–40 mm, although media down to 5 mm are sometimes encountered. As a general rule, the size of media has to match the size of material being ground: large media can’t produce the ultra-fine particles required in the finished cement, but small media can’t break large clinker particles. Mills with as many as four chambers, allowing a tight segregation of media sizes, were once used, but this is now becoming rare.

-Procyon Mukherjee

Concrete

Cement Makers’ Margins To Fall Rs 50-75 Per Tonne Amid West Asia Conflict

Crisil Sees Margins Easing Despite Steady Demand

Concrete

UltraTech Board Approves Rs 50 bn Fundraise Via NCDs

Company to issue half a million debentures for expansion plan

Concrete

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Line-2 expansion to make Kadapa a major cement hub

Cement Makers’ Margins To Fall Rs 50-75 Per Tonne Amid West Asia Conflict

UltraTech Board Approves Rs 50 bn Fundraise Via NCDs

Fornnax Names Lukas Baur as Authorised Service Partner to Bolster EU Operations

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Cement Prices to Stay Flat in Q2 FY27 as Costs Squeeze Margins

Cement Makers’ Margins To Fall Rs 50-75 Per Tonne Amid West Asia Conflict

UltraTech Board Approves Rs 50 bn Fundraise Via NCDs

Fornnax Names Lukas Baur as Authorised Service Partner to Bolster EU Operations

Lokesh Lays Stone For Rs 31 Billion Cement Unit In Kadapa

Cement Prices to Stay Flat in Q2 FY27 as Costs Squeeze Margins

-

Concrete1 month ago

Concrete1 month agoJK Cement To Target Higher Capacity Utilisation And Premiumisation

-

Concrete1 month ago

Concrete1 month agoCement Prices To Hold Steady Amid Monsoon Slump

-

Concrete1 month ago

Concrete1 month agoJK Cement Plans To Boost Capacity Utilisation And Premiumisation

-

Concrete3 weeks ago

Concrete3 weeks agoNuvoco Vistas launches Limla cement plant, expands Gujarat footprint