Concrete

Cement Volume Set to Rise to 450MT by FY25 with Rising Infrastructure

As the infrastructure and real estate industry is set to upcycle, CareEdge reports a boost in demand for cement and shares its projection on expected growth.

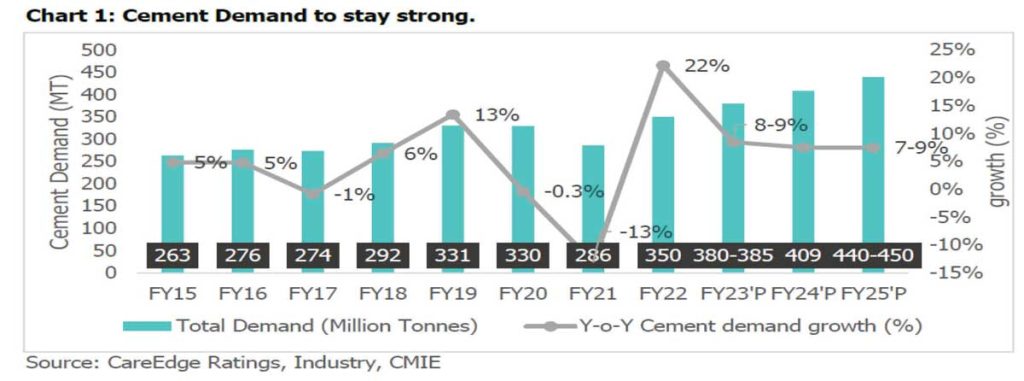

The cement industry has benefitted from high volume growth, majorly driven by a revival in demand from the housing sectors, upcoming infrastructure projects such as the construction of roads, railways, and highways as well as generous rural demand. The cement sector remains one of the key beneficiaries of economic growth as there is a positive correlation between GDP growth rate & cement demand growth. In the 9MFY23, the overall cement demand registered 11 per cent growth over last year and on a full year basis CareEdge expects 8 per cent to 9 per cent growth.

The central government continues to focus on increasing capex outlay to spur growth in light of the 2024 general elections. The capex for 2023-24 (Budget Estimate) at Rs 10 lakh crore is almost 3 times of the capital expenditure in FY2019-20. The capex spree also augurs well with the central government’s aim to make growth more inclusive as investment in infrastructure and productive capacity have a multiplier effect. The public sector capex has focused on improving the connectivity inside the country and gradually the allocation for highways and railways have surged from 35 per cent in FY18 to 43 per cent in FY23. The Union Budget 2024 also increased outlay on railways and plans for 50 new airports.

The combined effect of increasing infrastructure spends, real estate upcycle, low per capita consumption and the expected increase in private sector capex well supports the demand growth for cement in FY24-FY25. CareEdge expects the sales volume for the cement industry to grow by 8-9 per cent in FY23 to 380-385 MT and to 440-450 MT by FY25 year-end with Central and eastern regions witnessing more lucrative demand. Given the demand is expected to remain robust in upcoming years, the cement players have also announced additional capacity to keep up with the growth pace.

The cement industry is concentrated with the top 10 players having more than 68 per cent of the installed capacity share. Going forward as well the capacity expansion during FY23-FY25 is expected to be predominantly undertaken by the top players and hence the consolidated nature of the sector is likely to continue. “The sector may also witness acquisition of mid or smaller-sized players by the top players amid the prolonged margin pressure which the sector is witnessing. This will lead to further consolidation in the sector and better pricing discipline amongst remaining players,” said Ravleen Sethi, Associate Director, CareEdge.

Concrete

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Executive named to succeed current managing director in 2027

Concrete

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Rs 273 crore purchase broadens the developer’s Pune presence

Concrete

Adani Cement and Naredco Partner to Promote Sustainable Construction

Collaboration to focus on skills, technology and greener practices

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!

World Cement Association Annual Conference 2026 in Bangkok

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!