Concrete

Structural Shift in the Cost Curve

The cost curve in the Indian cement industry has been on an upward trajectory. ICR delves into the causes behind it and its impact while endeavouring to answer the important question – how much of this is permanent?

If the financial year 2022 was the year of shipping costs soaring to the highest level, the financial year 2023 started with the coal and pet coke prices moving to the stratosphere in tandem, largely buoyed by the geo-political headwinds with the war in Ukraine, forcing a sanction of a large part of the oil, gas and coal from the Russian sources to the Western world. The fallout of this was a steep hardening of the coal futures, both New Castle and API4 Indexes shot up to the extreme levels it has never seen in the past. While these

were FOB prices, the shipping freight, albeit softening from the stratospheric levels, were still high by any standard.

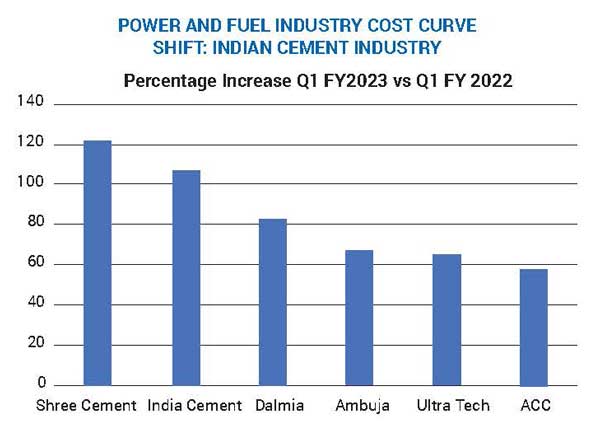

The Indian cement industry was hugely impacted by the rise in power and fuel prices as this contributes to 30 per cent of the industry cost of producing and distributing cement, the logistics cost still remaining high at 40 per cent of the total costs. The first quarter of FY2023 saw an across the industry rise of above 60 per cent in the power and fuel cost as attached in the graph below (compiled from the quarterly reports of the key industry players).

Market Dynamics

This rise has however cooled down in the recent quarter, but a large part of the rise seems to be permanent and the total shift in the industry cost curve is expected to be 20 per cent higher on power and fuel cost together with the impact of logistics cost. How do we explain this structural shift in cost?

While most of the analysis is based on the spot prices of coal, both in the international and domestic market, which in turn influences the prices of pet coke as well, the private buyers of coal and pet coke do not trade on spot basis for the bulk of their portfolio, which is built on an optimised model for buying a mix of domestic coal (linkage auction, e-auction and market coal), imported coal (RB1,2,3, Indonesian, other sources, etc), domestic pet coke (Nyara, Reliance, IOCL, etc), imported pet coke (U.S. East Coast, Oman, LATAM, etc), such that the landed cost could be minimised on the basis of rupee per kcal (heat value) as the portfolio must be normalised over the range of GCV options.

Private sellers and buyers have experienced in their own way through tenured contracts that inter-dependence in a highly volatile market did demonstrate better results over the long run, but in the short term both sides have engaged in short term opportunism. This has put additional strains in the system and these postures have influenced the spot prices. While the FOB prices started to show distinct ‘out of bound’ movement, the shipping costs remained high throughout this period and only recently have shown a definitive downward trend.

The individual cement players within the industry have very different portfolio of their own, built through the years on an optimisation programme that takes into account the kiln characteristics as well, in accepting a mix of coal or/and pet coke from a myriad of sources, where logistics cost becomes a very dominant factor; with shipping costs soaring, the negative results have been more pronounced for those who have an over-exposure to importation.

One of the important points to be noted is that the Indian coal prices have also gone up by 75 per cent on an average across a range of grades, those who have long term auction linkages still alive, are the outliers benefitting the most. The future direction of the domestic coal prices does not seem to portray a large change as most of the mines have a rising cost to contend with, as stripping ratios continue to rise every year, followed by logistics cost.

Taking on Challenges

The question of power and fuel cost rise should be seen in the long term rather than in the short term, although finding the most optimised mix in terms of cost has remained the area of focus all along. Two of the biggest challenges that urgently require solutions from the industry are as follows:

- Cement industry cannot continue to increase the use of fossil fuel in the mix of inputs: Apart from the emission issue that weighs on the situation (potential abatement costs included), the economics of higher fuel usage weighs far more menacingly on the cost curve. As every linkage auction quantity allocated to the cement industry has been steadily going down, it is expected that the prices will be moving up. The overall allocation still remains highly skewed to the power sector (where cement CPPs also become strong contenders), the overall situation after factoring in logistics issues still show that the domestic coal cost per MW of output has been rising steadily.

- Captive coal mines have remained a challenge in terms of overall cost: The only solution for the long term is to look for captive coal mines that have logistics advantages and where the costs over the long term can be found as a viable option when compared with other sources of coal or pet coke. But the actual progress on the ground is low due to the challenges of stripping ratios for the mines that are on offer.

- Pet coke prices have reasons for moving up: The US refineries have stopped all further investments and the portfolio is also getting transformed as far as their waste outputs are concerned. In the hierarchy of waste outputs, the total cost including the future abatement costs are increasingly being considered. In this regard, pet coke costs are likely to almost double if these considerations are factored in.

The structural shift of power and fuel price hypothesis can be tested in the next two quarters when the India cement industry would showcase their alternate hypothesis (use of Russian coal, Venezuelan pet coke). But the rise would still be significant over the long-term power and fuel prices that the industry witnessed, which used to hover around Rs 1000/T. Today, this is around Rs 1700/T for the industry, a shift which has happened in just two years’ time.

The question then shifts to whether the industry could create a structural pass-through of these costs in prices. With the current trajectory of prices, it does not seem to be happening. However, the industry is moving through a spate of consolidations and the recent entry of Adani could change the picture further. Its strong network advantages stemming from logistics consolidation across the entire geography of India could be a strong contender to challenge the current hypothesis.

– Procyon Mukherjee

Concrete

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Executive named to succeed current managing director in 2027

Concrete

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Rs 273 crore purchase broadens the developer’s Pune presence

Concrete

Adani Cement and Naredco Partner to Promote Sustainable Construction

Collaboration to focus on skills, technology and greener practices

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!

World Cement Association Annual Conference 2026 in Bangkok

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!