The Indian cement industry, has, over the years, employed the best available technology for production. Given their high degree of blended cement usage, Indian cement producers are at the forefront of both fuel and electrical energy consumption on a per tonne- of- product basis.

The Indian cement industry today, enjoys pride of place, being the second largest cement producer in the world. It has made rapid strides, not only in capacity addition but also in producing world-class quality cement from state-of-the-art technology. The industry currently accounts for about 7 per cent of the global production. On the energy front, the industry has proactively responded to the initiatives of the Bureau of Energy Efficiency in improvement of and reduction in energy consumption and some of the Indian plants have become global benchmarks in energy consumption, second only to Japan. The industry has also contributed significantly to the eco-friendly use of industrial wastes, thereby reducing its carbon emission. It currently consumes around 27 per cent of fly ash generated from thermal power plants, an environmentally hazardous waste and almost hundred per cent slag generated by the steel industry.

NA Viswanathan, Secretary General, Cement Manufacturers’ Association says, "The current economic slowdown has inevitably left a severe dent in the growth of the cement industry. The decline of the cement industry from an average growth of around 8 per cent to 9 per cent in the last couple of years to the present low of five per cent has shown no sign of improvement in capacity utilisation and this is still a major cause of concern. Currently, the demand-supply situation of cement is highly skewed, with the latter being significantly higher by over 90 million tonnes since the cement demand projections made by the government earlier have not materialised."

"Cement consumption has grown by about five per cent in FY2012-13 as compared to 7.1 per cent in FY2011-12. The demand growth in most of the regions is either declining or stagnating, with very few pockets of positive growth. Demand in the June quarter also remained weak due to early and heavy monsoons across India and poor infrastructure related growth," says Sumit Banerjee, Vice Chairman, Reliance Cement. Sumit adds, "The cement industry should bounce back in the next couple of years." According to RP Gupta, Chairman and Managing Director, Shiva Cement, substantial capacity was added in the recent past, in anticipation of a growth in demand. Gupta then goes on to say, , "Unfortunately, demand remains sluggish due to the slowdown in infrastructure and economy as a whole. However, such cyclical effects have been witnessed in the past,too. The cement industry being a core sector, the medium and long- term view should be taken, and that is certainly promising. Demand growth will definitely bounce back and excess capacity will bottom out in the next two years. Then again, new capacity additions are becoming difficult due to regulatory hurdles in land acquisition, mining leases and environmental approval. If these issues are not addressed, it can create a huge shortage and price hikes."

Speaking about the logistics issues, Gupta adds, "The logistics costs in our country are too high. Inadequate capacity in railways aggravates the problem for long- distance despatch of bulky product like cement, coal and minerals. In the larger interest of the country, we must transfer the traffic of goods by road to the railways; this is cost-efficient and reduces the burden of imported energy. This needs a major restructuring of railway and augmenting investment of Rs.12 lakh crore in the 12th Plan, as against the Rs 2.6 lakh crore of the 11th Plan."

Speaking about some of the challenges the industry faces, Pawan Ahluwalia, Managing Director, KJS Cement had this to say: "Taxation is highly skewed for cement; we would like to see a rationalised tax structure. Another issue is that the demand-supply scenario is out of sync, yet major players are into augmentation of capacity. The input costs have gone up; the logistic costs are heading north, as also overhead costs. These are impacting an industry which is still in consolidation mode. So, the growth of the cement industry, as per my understanding, is going to be about 11 to 12 per cent, as has been projected by the Planning Commission."

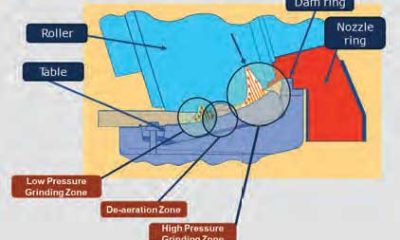

Voicing his concern about the lack of support from the government at policy level, Alok Sanghi, Director, Sanghi Industries, says, "The excise duty on steel is just four per cent, whereas for cement it is 12 per cent. My question is, why should there be such a difference in duty between two building materials which are used for the same purpose? Ultimately, the cost of housing is increasing because of the increase in taxes. If you look at the ex- factory cost of cement and if you add the taxes we are paying, it is equivalent to luxury goods, and cement is essential goods. So I think the government really needs to focus on how they can reduce the cost of cement, either by reducing the royalties or reducing the excise duty, VAT, etc. My view is, the most important thing the government can do is to increase the percentage spend on infrastructure development. For example, China spends almost 12 per cent of its GDP on infrastructure development whereas India spends less than five per cent. So, if the government increases its infrastructure spend, it will automatically have a huge impact on the demand for cement and that obviously will help in capacity utilisation." Speaking about the technological advancement in the industry, Bidyut Bhattacharya, Technical Director, Sinoma International Engg Co India says, "The Indian cement industry, over the years, has employed the best available technology for production. Thanks to a high degree of blended cement utilisation, Indian cement producers are at the forefront of fuel and electrical energy consumption on a per tonne- of- product basis. An additional benefit in terms of sustainability is the lower per tonne CO2 emission. Stricter regulatory requirements are leading to greener technologies, and they in turn, lead to further energy efficiency." According to him, utilising a vertical roller mill or roll press circuit in finish grinding mode for raw material grinding is the industry norm today, and this makes for a significant energy cost reduction when compared to the traditional closed circuit ball mill system. Likewise, for coal grinding, a vertical mill is used, and for the energy- intensive finish grinding process, the ball mill plus roll press system is widely popular. In specific cases where slag grinding is involved with high percentage moisture, the VRM technology for finish grinding is used. Only in extreme cases do we get a request for close circuit ball mill for grinding, this is inherently less energy- efficient. High efficiency separators are the standard today for all milling systems."

Bidyut adds, "As regards the pyro-processing area, Indian cement producers continuously strive to achieve the lowest specific fuel consumption along with high power savings. High efficiency fourth- generation grate coolers are being widely used; they provide high recuperation efficiency along with lower maintenance interventions. As the total cooling air requirement reduces from the earlier 2.2Nm3/kg clinker to say, 1.8Nm3/kg clinker, there is a lot of savings through reduced exhaust air and fans` power consumption.

To achieve lower fuel consumption, six stage pre-heater systems are the popular choice, along with in- line calciners. Advanced low NOx technologies are used in many cement plants. As regards process fans, a static efficiency = 82 per cent and use of variable speed drives reduces power consumption."

According to him, however, there is scope for improvement, especially with regard to waste heat recovery systems which is slowly catching on in India. Bidyut says, "It is imperative to make WHR a mandatory requirement for any new cement plant, as is the case in some emerging countries. A significant portion of the energy requirement can be sourced through utilisation of waste heat from the pre-heater and cooler. In this context, Indian cement producers/consultants need to do a more specific, case- to- case basis, cost- benefit analysis for the six stage vs. the five stage pre-heater system, specifically when raw material moisture is high or when civil design parameters like wind speed/seismic conditions are not favourable. Also, these days, the usage of alternate fuels in cement processing is quickly picking up.

Considering the dwindling quality/supply of domestic coal and the logistic issues of imported supply, a variety of alternate fuels are being utilised cost- effectively; not only pet coke but a host of other materials from tyres to rice husk, plastic, sawdust, are all being used. Utilisation of municipal wastes/ sludge is still in its infancy in India, primarily due to supply- side bottlenecks."

Bidytu ends, saying, " It is worthwhile to mention here that cement pyro-processing systems are highly suitable for burning waste materials, apart from contributing to the calorific value, because of some pertinent factors: the very high incineration temperature, close to 1,800 to 2,000 deg C at the flame zone, the higher residence time, say five to six seconds in calciners, the assimilation of heavy metals in the clinker, negligible dust emissions through the kiln bag filters and the dry dust curtains with high surface area in the pre-heater which scrubs the gases of pollutants."