Concrete

Strong-linking the Supply Chain

Innovation of distribution channels and logistics solutions is the key to making cement more profitable. Since cement is a low-cost, high-volume commodity, its distribution is a major cost driver for the manufacturers. ICR delves into the current trends in logistics as it is the most price- and time-intensive element in the supply chain of cement in India.

Logistics for cement begins from the source where limestone, the raw material, is procured from mining sites and brought to the plant. Logistics ends with the finished product leaving the manufacturing facility and ultimately reaching the consumer. For this, it travels across the length and breadth of the country. The demand for cement by every organisation must be met on time, or they lose the opportunity to their market competitors. The mode of transport for cement decides its cost and generally holds up to 20 per cent of its retail price. The cement industry today uses multiple modes of transportation to fulfil its logistical needs.

According to Cement Manufacturers Association of India (CMAI), the Indian cement industry is the second largest revenue source of the Indian railways with a contribution of US$1.2 billion per annum in freight revenue. To make it a more economical and accessible government of India has launched schemes like long term tariff contract scheme, freight incentive scheme, incentive scheme for auto traditional empty flow directions and general-purpose wagon investment scheme. These schemes have encouraged cement companies to sign contracts with the railways. Roadways is also largely used for transporting cement in fleets of trucks from the manufacturing plants to the distributors, dealers, and franchises.

Creating a strong network

Largely there are three contenders in the distribution channels – wholesalers, retailers and end consumers. Cement organisations sell their end product to the consumers through wholesalers or retailers. With changing times and demands, companies may create a system to sell to their end consumers directly using the internet.

The distribution channels for cement can vary depending on the market and location, but generally, there are a few common channels through which cement is distributed:

- Direct sales to construction companies: Cement manufacturers often sell their products directly to construction companies and contractors who use the cement in their projects.

- Distributors and wholesalers: Cement manufacturers may also work with distributors and

- wholesalers who purchase large quantities of cement and resell it to smaller retailers and construction companies.

- Retailers: Retailers such as home improvement stores, hardware stores, and building supply stores also sell cement to consumers and small contractors.

- Online sales: Some cement manufacturers and retailers offer online sales and delivery services, allowing customers to purchase cement and have it delivered directly to their construction site.

- Export: Cement manufacturers may export their products to other countries through international trade channels, such as shipping companies and international distributors.

- Overall, the distribution of cement can involve a complex network of manufacturers, distributors, wholesalers, retailers, and exporters.

The cost factor

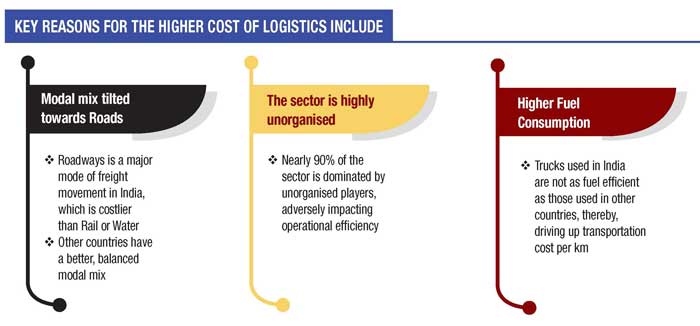

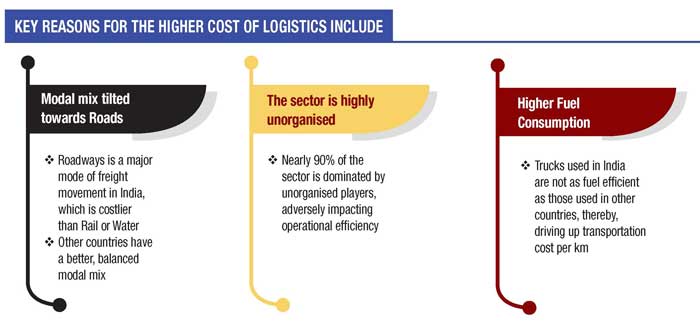

According to a Logistics Report published by Motilal Oswal Investment Services in March 2023, India’s logistics cost to GDP ratio hovers around 13 per cent 14 per cent as compared to 8 per cent to 10 per cent for other major economies. The high cost of logistics in India has been due to an inefficient modal mix, owing to a relatively inefficient road segment. More than 70 per cent of the freight movement in India is via road as compared to 44 per cent in China, 45 per cent in Europe and 39 per cent in the US.

Automated Guided Vehicles can help automate

the movement of materials within warehouses

and production facilities, reducing labor costs and

improving efficiency.

In order to bring the overall logistics costs of India to competitive levels, the Government of India has formulated the National Rail Plan (NRP), where the share of Indian railways in the overall modal mix is envisaged to increase to 40 per cent (~18 per cent in 2020) by 2031. Further, with dedicated freight corridors getting operationalised in phases, the market share for rail would likely increase in the modal mix.

Pushpank Kaushik, CEO, Jassper Shipping, says, “Since commodities such as cement are transported in bulk, the freight cost for cement rises and railways are the favoured method of transport for bulk commodities because roadways are impractical. However, railways present their own set of freight transport difficulties. The main issue raised by cement industry participants, particularly the small plants, is the difficulty in obtaining railway rakes or wagons, particularly during peak/seasonal periods. The fluctuation of power, fuel, and diesel has a significant effect on freight costs. As a result of these difficulties, India’s logistics costs account for 13-14 per cent of overall GDP, compared to 7-8 per cent in developed nations.’’

According to Teamlease Regtech, India’s leading Regulatory Technology (Regtech) solutions company’s report titled ‘Simplifying Compliance Management for The Logistics & Supply Chain Industry’, the logistics industry in India employs 22 million people and is on track to reach a valuation of $215 billion in the next two years. The National Logistics Policy (NLP) was recently introduced to address the infrastructure and policy gaps in the industry. The objective of this policy is to reduce the cost of logistics from the current 14 per cent of GDP to 8 per cent of GDP by 2030. In addition, there has been a renewed focus on implementing technological solutions to push paperless trade operations and place India within the top 25 on the Logistics Performance Index (LPI).

The report also reveals that three major regulations of the industry, such as the Multimodal Transportation of Goods Act of 1993, the Carriage of Goods by Road Act of 2007, the Carriage of Goods by

Sea Act of 1925, the Merchant Shipping Act of 1958, and the Carriage by Air Act of 1972 all

required updation.

Rishi Agrawal, CEO and Co-Founder, Teamlease Regtech, says, “A robust logistics and supply chain industry is the key for India’s transformation as the factory of the world. The report looks into the logistics industry’s regulatory environment to provide readers with an understanding of the complexities of the compliance landscape. It highlights the limitations and inefficiencies in the current compliance practices used by these businesses. It also makes recommendations that will allow these businesses to efficiently manage their compliance requirements through the use of digital procedures.”

More than 70 per cent of the freight movement in India

is via road as compared to 44 per cent in China, 45 per

cent in Europe, and 39 per cent in the US.

Technology: The saviour of logistics

Technology can play a significant role in optimising the logistics function of the cement industry in India. Following are the ways in which technology can be integrated into the operations of the cement industry:

- GPS tracking: Cement companies can use GPS tracking technology to monitor the location and movement of their trucks carrying cement. This helps them track delivery times, optimise routes, and reduce fuel consumption.

- Warehouse management systems (WMS): Implementing WMS software can help companies better manage their inventory, reducing storage costs and minimise stockouts.

- Electronic Data Interchange (EDI): EDI can help cement companies exchange business documents with their partners electronically, reducing the need for paper-based communication and improving the efficiency of the supply chain.

- Predictive analytics: Predictive analytics can help cement companies forecast demand and optimise their production and distribution schedules, reducing waste and improving customer satisfaction.

- Automated guided vehicles (AGVs): AGVs can help automate the movement of materials within warehouses and production facilities, reducing labour costs and improving efficiency.

- Blockchain technology: Blockchain technology can help improve transparency and traceability in the supply chain, reducing the risk of fraud and counterfeiting.

By leveraging these technologies, cement companies in India can optimise their logistics function, reduce costs, and improve customer satisfaction, ultimately enhancing their competitiveness in the market.

“Today, the way digitisation is happening across the world, it is bringing a good amount of visibility across different segments in any organisation. While you talk about logistics, which is the last mile towards delivering the finished goods to a customer, it is very important that manufacturing works in tandem with it. This will work if you have the right technology and if you want to scale, have more visibility and give your customer a good experience. Technology is the backbone, which will help you achieve all this. If you are looking at a 10x or 20x growth in a duration of three years, you need to scale up through technology,” say Sunil Kharbanda, CRO and Co-Founder, Trezix Software.

Achieving efficiencies

The Indian cement industry is going green. While they are resorting to alternative fuels and raw materials to achieve sustainability in their productions, logistical operations can achieve sustainability by using alternative fuels for their vehicles, optimising the routes for their carriers, adopting green packaging of product, implementing green warehousing and encouraging their vendors to procure their product in a greener fashion. By incorporating sustainability in their logistics operations, the Indian cement industry can reduce their environmental impact, improve their reputation, and gain a competitive advantage in

the market.

According to the spokesperson at Dalmia Cement (Bharat) (DCBL), green initiatives or ESG is increasingly crucial for companies, especially in hard-to-abate sectors. As part of their ESG initiatives, they are committed to reducing the emissions footprint of their operations and that includes road logistics. DCBL has introduced LNG and EV trucks as part of their green logistics strategy for the decarbonisation of its transportation fleet, which accounts for around 1.5 per cent of total CO2 equivalent emissions. They have tied up with various players in the logistics sector for supply of greener transport. Some of these vehicles are already being used for transportation for inward and outward movement of raw materials and manufactured goods in their different plant locations. The current consignment of 35 LNG trucks is also one of the biggest in the cement sector. DCBL is planning to convert 10 per cent of their existing fleet of 3,000 vehicles to the eco-friendlier LNG and EV, alternative transport by end of FY24.

Optimisation of logistics freight costs is a critical area for the Indian cement industry, as logistics costs can account for a significant portion of their overall operational costs.

Here are a few strategies that cement companies in India can adopt to optimise their logistics freight costs:

- Multi-modal transportation: Cement companies can use a combination of transportation modes such as road, rail, and sea to minimise transportation costs and reduce transit times.

- Collaborative logistics: Cement companies can collaborate with other manufacturers to share logistics resources and reduce costs.

- Real-time tracking and monitoring: Using real-time tracking and monitoring systems can help companies optimise routes, improve delivery schedules, and reduce transportation costs.

- Consolidation of shipments: Cement companies can consolidate shipments to reduce the number of trips required and achieve better economies of scale.

- Negotiation of rates: Cement companies can negotiate rates with logistics service providers and carriers to get the best rates and terms.

- Optimisation of inventory: Cement companies can optimise their inventory levels and use just-in-time (JIT) inventory management techniques to reduce transportation and storage costs.

- Use of advanced technologies: Technologies such as AI, machine learning, and predictive analytics can help cement companies optimise logistics freight costs by predicting demand, identifying opportunities for cost savings and streamlining operations.

By adopting these strategies, the Indian cement industry can optimise their logistics freight costs, reduce operational expenses and improve their bottom line.

“Digitising proof of delivery and freight invoicing is something I have never seen before. Not only for the cement companies, but everyone who works in the value chain, the trucker, the logistics provider, the transporter, each one of them can benefit from this and that would be a big change and step to remove paper trails and make them as digital records. When we think about EPOD and digital freight invoicing that you do at the end of the day ensures all stakeholders are benefited from it. Cement companies have contracts with logistics providers or transporters or they sometimes hire fleet owners and trucks from the market if they do not have their own. Any solution or change ultimately needs to impact life like everyone in the ecosystem.

EPOD and digital freight invoicing achieves just that by easing the operations for everyone,” says Swapnil Shah, Founder and CEO, Freight Tiger.

The Indian cement industry has a complex network of distribution channels, which includes direct sales to construction companies, wholesalers, retailers, and online sales. The industry can also leverage innovative technologies to optimise logistics operations and improve sustainability. To optimise freight costs, the Indian cement industry can adopt various strategies, and advanced technologies like AI and predictive analytics. By implementing these strategies, the industry can reduce costs, increase efficiency, and gain a competitive edge in the market. In sum, the Indian cement industry has great potential to leverage innovation and optimise logistics to overcome challenges and grow sustainably in the future.

-Kanika Mathur

Concrete

NDMC Rolls Out Intensive Sanitation Drive Across Lutyens Delhi

Municipal body intensifies cleaning and monitoring across the capital

Concrete

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Executive named to succeed current managing director in 2027

Concrete

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Rs 273 crore purchase broadens the developer’s Pune presence

NDMC Rolls Out Intensive Sanitation Drive Across Lutyens Delhi

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!

NDMC Rolls Out Intensive Sanitation Drive Across Lutyens Delhi

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction