Concrete

The Add-On Effect

Hetal Gandhi, Director – Research, and Koustav Mazumdar, Associate Director, CRISIL Market Intelligence and Analytics discuss the increased budget outlay for infrastructure to boost cement demand and to rapidly develop the east and central regions of the country.

The domestic cement industry has been in high demand over the past fiscal or so.

A rush of government spending on infrastructure has boosted consumption of this key commodity.

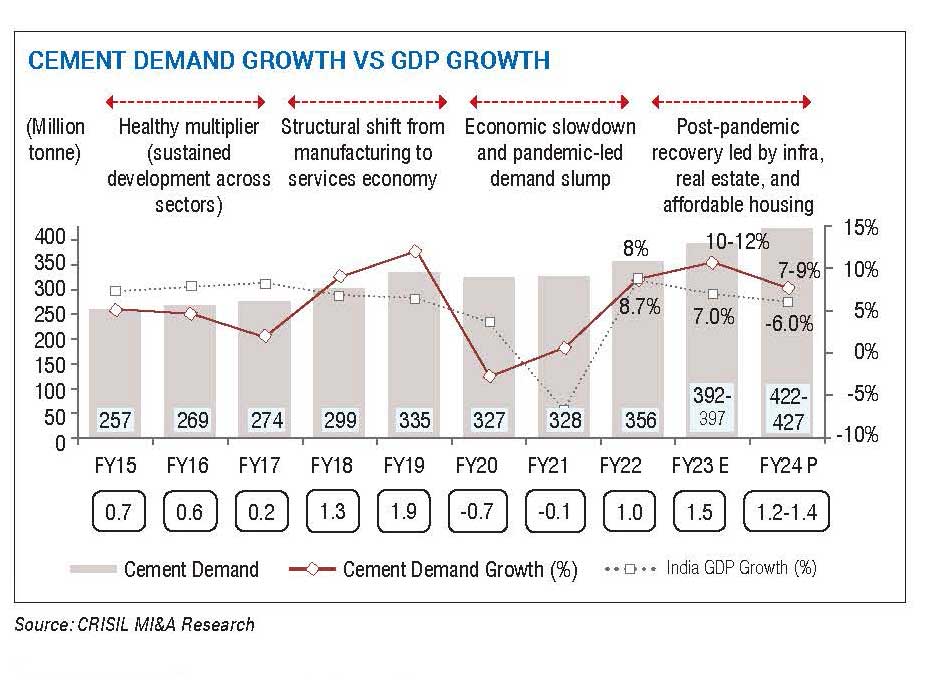

Demand for cement increased ~8 per cent in fiscal 2022, followed by ~11 per cent growth in the first 10 months of this fiscal. Sustained demand momentum in the last quarter of the current fiscal is expected to peg demand growth at 11 per cent for the full fiscal on a high base of the previous fiscal.

The infra-focused budget, presented on February 1, will ensure the momentum continues into the next fiscal.

A ~33 per cent rise in budgeted capital expenditure to Rs 10 lakh crore for fiscal 2024, and weighty allocations to infrastructure sectors such as roads and affordable housing augur well for cement demand, which is projected to rise 7-9 per cent to ~425 million tonnes in the fiscal.

The GDP Correlation

Rise in cement demand correlates with gross domestic product (GDP) growth as economic development requires heavy investments in infrastructure such as housing, roads, ports, etc.

The cement demand growth to GDP growth multiplier (i.e., cement demand growth divided by GDP growth in the same year) witnessed an unprecedented drop in fiscals 2020 and 2021, because of the pandemic-caused economic slowdown, but recovered rapidly in fiscal 2022, with cement demand and GDP rebounding at a similar rate.

This fiscal, the multiplier is expected to pick up pace as demand growth accelerates and GDP growth moderates on a high base. We expect the multiplier to remain >1, but to decrease marginally next fiscal, as cement demand increase moderates to 7-9 per cent on a favourable base, while GDP growth slackens to ~6 per cent because of global economic slowdown, transmission of interest rate hikes to consumers (leading to weakening industrial activity), and as the catch-up in contact-based services fades.

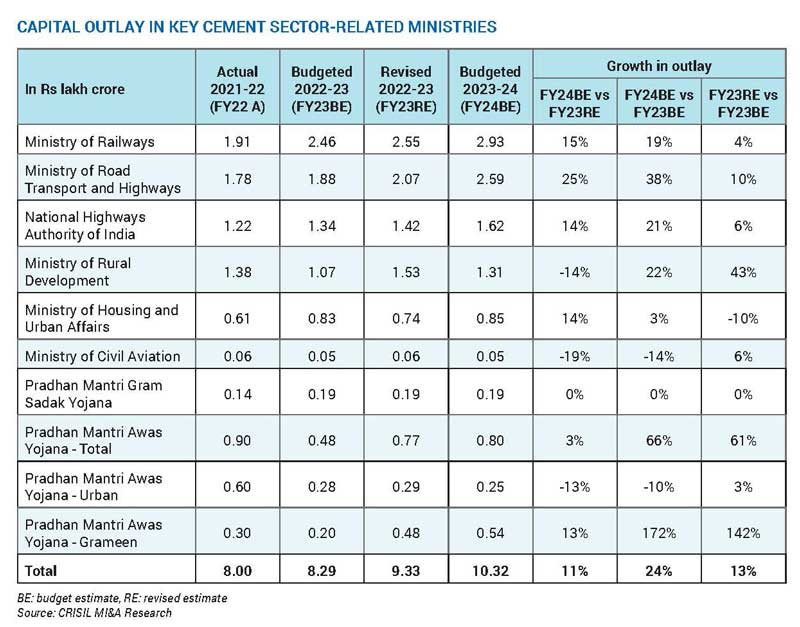

Budget announcements indicate a robust ~20 per cent increase in capital outlay for ~13 key construction-heavy ministries for fiscal 2024. Higher allocation to cement-heavy sectors, accelerated infra execution ahead of elections, and traction in rural affordable housing are expected to lead to 7-9 per cent rise in demand next fiscal on a high base of two consecutive years. This translates to ~30 per cent rise when compared with the pre-pandemic levels and a 9-10 per cent CAGR between fiscals 2022 and 2024.

The Ministry of Road Transport and Highways (MoRTH) and the National Highways Authority of India (NHAI) have received 25 per cent and 14 per cent more allocation, respectively, in fiscal 2024BE against fiscal 2023RE, despite overachieving fiscal 2023BE targets by ~10 per cent and ~6 per cent, respectively.

The allocation for Pradhan Mantri Awas Yojana (PMAY), which includes urban and rural housing, increased 3.2 per cent for fiscal 2024 against fiscal 2023RE. Compared with fiscal 2023BE, however, the revised estimate has seen ~60.7 per cent increase to Rs 0.79 lakh crore.

Allocation under the PMAY-Gramin scheme had been increased last fiscal, with the total expenditure rising to Rs 0.48 lakh crore after an initial allocation of only Rs 0.2 lakh crore in the 2022-23 budget. The government approved an additional Rs 0.18 lakh crore in November 2022, which will also aid demand growth in the first half of the upcoming fiscal.

However, allocation under PMAY-Urban is set to decline this fiscal as it draws to a close with over 1.08 crore units either completed or nearing completion, out of the sanctioned 1.23 crore units. Finally, though there is no change in the Pradhan Mantri Gram Sadak Yojana (PMGSY) allocation (at Rs 19,000 crore for the second consecutive year), there is no reduction in expenditure either. Also, 50 additional airports, heliports, waterdromes and advanced landing grounds have been proposed for improving regional air connectivity.

All of this will boost the already sturdy demand for cement in the upcoming fiscal.

As the capital outlay indicates, infrastructure will remain the key demand driver for the cement sector, led by government spending on roads, housing, urban infra, etc.

Rural housing demand is expected to grow at a healthy rate as well on the low base of last fiscal, increased allocation under PMAY-G, and healthy rural income owing to increase in crop prices. However, the weather and monsoon will bear watching.

On the other hand, urban housing demand is expected to moderate with the PMAY-U scheme coming to a closure, and a downward slide in real estate due to surging interest rates and high

capital values.

The industrial/commercial segment will continue to support demand growth amid capital expenditure push by large players, implementation of the production-linked incentive scheme, return to office/hybrid model of working, and overall economic recovery.

The Regional Landscape

Higher traction under PMAY-G, NHAI, and PMGSY will drive demand in the high-growth east and central regions. Around 3.4 million units are under construction in these regions as of January 2023 under the PMAY-G scheme.

Region-wise, demand growth is likely to be sharper in central and eastern regions, which account for ~80 per cent of PMAY-G construction and ~41 per cent of NHAI target set for fiscals 2020-2024. A favourable base, low per-capita cement consumption, and a big housing shortage will propel demand and keep utilisation levels stable in these regions, given aggressive capacity additions planned there.

South is lined up to follow central and east regions thanks to higher targets under Bharatmala Pariyojana, sharper execution under PMAY-Urban, and boost from realty and irrigation projects.

North India is expected to witness moderate growth on a high base, but various infrastructure projects — roads, metros, dedicated freight corridors, etc — and pick-up in real estate will support growth in the region.

In the west, demand is projected to grow at a moderate rate in the near term after rebounding sharply last fiscal. This region has various high-budget infra projects under execution, such as the Mumbai-Ahmedabad bullet train, trans-harbour link, and metro projects in Mumbai. However, north, south and west, comprising industrialised states, already have the highest per-capita cement consumption, which will limit their demand growth potential and will lag the other two regions in the future.

ABOUT THE AUTHOR:

Hetal Gandhi, Director – Research, CRISIL Limited, is managing a team of over 20 analysts to track developments across infra and consumption space to know India’s role in this journey.

Koustav Mazumdar, Associate Director – Metals, Metallurgical Coal, Cement and Hydrogen,

CRISIL Limited.

Concrete

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Executive named to succeed current managing director in 2027

Concrete

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Rs 273 crore purchase broadens the developer’s Pune presence

Concrete

Adani Cement and Naredco Partner to Promote Sustainable Construction

Collaboration to focus on skills, technology and greener practices

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!

World Cement Association Annual Conference 2026 in Bangkok

UltraTech Appoints Jayant Dua As MD-Designate For 2027

Merlin Prime Spaces Acquires 13,185 Sq M Land Parcel In Pune

Adani Cement and Naredco Partner to Promote Sustainable Construction

Operational Excellence Redefined!