Concrete

Revisiting the Race to Net Zero

The supply of carbon capture pathways holds the key for the cement industry’s success of being carbon neutral.

The Inter-Governmental Panel on Climate Change (IPCC) in their seminal thesis, ‘Working Group III Report’, which is a lengthy document, has summarised in three parts the currency of climate change actions so far and the visible pathways to the future. Firstly, it has been pointed out that the supply of renewable energy solutions from photo-voltaic cells, on-shore and offshore wind, solar and battery for electric cars have grown, hastening the drop in their unit cost. But the rise of emissions and the stock of emissions have grown unabated, other than the year 2020, when due to Covid, there was a brief respite. In 2022, the rise in emissions is back again. Thirdly, the global pathways to the emission reduction do not portray a possibility of less than a 1.5oC rise in the end of 2100, in fact the pathways are showing a rise above 2oC, simply from the fact that the stock of emissions out there do not seem to be coming down despite all the pledges and actions.

The Report summarises, “Projected cumulative future CO2 emissions over the lifetime of existing and currently planned fossil fuel infrastructure without additional abatement exceed the total cumulative net CO2 emissions in pathways that limit warming to 1.5°C (>50 per cent) with no or limited overshoot.”

Industry by industry, including the most emitting ones, has the same story line, unless outputs come down, the per unit emission after a brief sojourn, stopped to become lower.

Take cement, the per tonne emission that came down from the level of 1t to 900kg (global average) has now stagnated, with some faring better, but the overall industry is still at the alarming level and if the world continues to produce 4 billion tonne per annum of cement, with volumes moving up as new cities and urbanisation progresses, the stock of emissions do not have an easy and quick solution to be regressed.

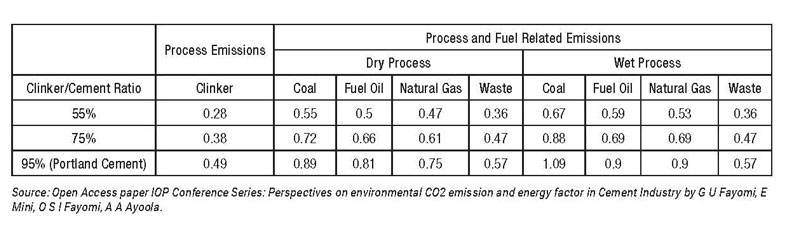

Calculating the emissions

The major industrial pollutant emanating from the manufacture of cement is the evolution of CO2, an estimated 40 per cent of the total CO2 generated from the industry, emanates from fossil fuel burning which is used in the production process, and another 50 per cent, from the raw materials utilised and the manufacturing process, and 10 per cent from indirect emissions by transportation of finished goods. For every 1kg of cement produced, 0.9kg of CO2 is evolved, and this equates to the evolution of about 3.6 billion tonnes of CO2 produced annually, and these figures don’t take into account the emissions from the quarrying and transportation of raw materials and the transport and delivery of produced cement.

The stages where these emissions occur are:

- The combustion of fossil fuel in the clinkering process to heat the raw material of limestone (CaCO3), produces CO2 at temperatures exceeding 1450°C.

- The calcination process (raw material conversion) in cement production process, also generates a significant amount of CO2.

- Indirect emission from transportation and delivery of raw materials and finished goods (electrification of vehicles shifts some of these pathways to more centralised use of renewable energy).

- CO2 generated from fossil fuel based electricity generation means, for running plants and equipment. It should however be observed that the amount of CO2 evolved in the manufacturing process also depends on:

- The type of manufacturing process adopted i.e. type of kiln used.

- The type of fuel used (pet coke, natural gas, coal etc.).

- The clinker/cement ratio i.e. percentage of additives.

CO2 emissions per kg of cement produced with several inputs used in the process reveals a picture as follows:

It is clear that the opportunities that existed within the mix of inputs and outputs (clearly Portland cement, known as OPC in India is a no-go going by the emission pathways), the industry has exercised the best mix to get to the current improvement in emissions, which still hovers around 900 kg per tonne of cement produced and some leaders are at 850 kg, while the laggards are at 940 kg.

This in itself would mean that lower clinker factor (slag cement, composite cement, PPC) will score over Portland cement and usage of slag (proximity to steel plants), fly ash (proximity to power plants), wet fly ash (proximity to fly ash ponds) and usage of wet fly ash and conditioned ash with freight incentives in rail have increased, thus taking us closer to the 850kg of CO2 emissions per ton of Cement output for some of the leaders in the fray. The efforts on efficiency improvement also seem to have stagnated after reaching a threshold.

The journey from here needs to look at carbon capture and sequestration as also observed by the IPCC Report. IPCC models require carbon removals to ramp up from 0.1 gigatons of CO2 today to an average of around 6 gigatons by 2050. Carbon removals work alongside emissions reduction solutions; they are not a substitute. But at the current pace, the pipeline of carbon removal projects will fall short of the volume of carbon removals the IPPC says is required in 2025 by 80 per cent.

What does this mean for the cement industry? What are the carbon capture and sequestration costs? How would these costs come down with development of new technology?

If one goes by the best available technology, removing CO2 from the atmosphere and recycling it to produce synthetic fuel forever is where some of the progress is happening and the current costs of $600/T is projected to move to $100/T. But this may not be economically feasible for cement, where the current average cost of producing cement itself is $75/T.

Looking ahead

The long term focus remains to be in the direction of carbon capture and storage for cement that would mean that concrete serves as the holistic Carbon sink in more ways than one. This would mean progressing on technologies that enable capture and utilisation of CO2 directly at cement manufacturing facilities; carbon mineralisation methods in which CO2 is captured and injected into fresh concrete where it becomes permanently embedded and actually helps improve its strength; and carbon storage in which CO2 is captured and stored securely in long-term geologic reservoirs (and not used for enhanced oil recovery).

Much of this would need clear investments and transparency is of paramount importance as every progress will attract more investment and only then can the costs come down.

Going by the current gaps in the progress for Net Zero, the investment gap for the Carbon Capture and Storage and Utilisation is where all the focus must shift. The days of glorifying the achievements in mostly exploiting the low hanging fruits is over.

-Procyon Mukherjee

Concrete

World Cement Association Annual Conference 2026 in Bangkok

Global leaders to focus on decarbonisation and digitisation

Concrete

Assam Chief Minister Opens Star Cement Plant In Cachar

New plant aims to boost local industry and supply chains

Concrete

Adani Cement, NAREDCO Form Strategic Alliance

Partnership to advance skills and sustainable construction

World Cement Association Annual Conference 2026 in Bangkok

Assam Chief Minister Opens Star Cement Plant In Cachar

Adani Cement, NAREDCO Form Strategic Alliance

Walplast’s GypEx Range Secures GreenPro Certification

Smart Pumping for Rock Blasting

World Cement Association Annual Conference 2026 in Bangkok

Assam Chief Minister Opens Star Cement Plant In Cachar

Adani Cement, NAREDCO Form Strategic Alliance

Walplast’s GypEx Range Secures GreenPro Certification

Smart Pumping for Rock Blasting

-

Economy & Market4 weeks ago

Economy & Market4 weeks agoBudget 2026–27 infra thrust and CCUS outlay to lift cement sector outlook

-

Economy & Market4 weeks ago

Economy & Market4 weeks agoFORNNAX Appoints Dieter Jerschl as Sales Partner for Central Europe

-

Concrete2 weeks ago

Concrete2 weeks agoRefractory demands in our kiln have changed

-

Concrete2 weeks ago

Concrete2 weeks agoDigital supply chain visibility is critical