Increasing focus on savings in energy consumption, stringent emission and pollution control norms, thinning bottom lines on one hand, and thanks to the Perform-Achieve-Trade Scheme, launched by Bureau of Energy Eficeny (BEE), most of the cement majors been inspired to innovate for ways and means, not only to reduce the energy consumption and the carbon footprint, but also to better cost efficiency. This has resulted in plant optimisation where energy and fuel efficient equipment and components play a pivotal role. INDIAN CEMENT REVIEW trains its thoughts on the latest developments.

EVEN THOUGH THE economic slowdown has adversely impacted the off take of cement, and to an extent, has dented the confidence of the equipment vendors, the long term growth potential is really tremendous. The per capita consumption of cement in India tells no other tale. Indian per capita consumption of cement is much less compared to the world average. As per reports, compared to the world average of over 350 kg, the Indian per capita consumption of cement was around 150 kg in 2011. The corresponding figure is 660 kg per capita in China, 631 kg per capita in Japan and 447 kg per capita in France. This very fact has been one of the main reasons that brought in global players into the Indian shore.

The Indian cement industry is globally competitive with lowest energy consumption and CO2 emissions. As per inputs from Cement Manufacturers Association during 2009-10, the Indian cement industry grew at a robust rate of 12.7 per cent. With the government promoting construction activities across the country through various stimulus packages for building roads, bridges, houses, etc., the Indian cement industry added a capacity of 37 million tonne in 2009-10, which is the highest capacity ever added in any single year so far. The government’s focus on building infrastructure is likely to continue in the near future and the Indian cement industry is expected to sustain an even higher growth rate of 15 per cent over the coming years.

According to G Jayaraman, Associate Director, Price Waterhouse, Chennai, the Indian cement industry has been very proactive in adopting various technological advancements taking place all over the world. This was particularly triggered by the partial decontrol of cement industry in 1982 followed by full decontrol in 1989 giving the resultant free market competition an opportunity for growth in production and productivity. Jayaraman points out, "The share of energy inefficient wet process plants had slowly decreased from 94.4 per cent in 1960 to 61.6 per cent in 1980. Thereafter, as a result of quantum jump in production capacities through installation of modern dry process plants as well as conversion of some of the wet process plants, the share of wet process has reduced to less than 5 per cent today. During the last two decades (80’s and 90’s), major technological advancements took place in design of cement plant equipment/systems basically in the following major areas – a) pre-calcination b) high pressure grinding c) automation in process control d) high efficiency particle separation and e) clinker cooling.

Technology Roadmap

These innovation resulted in sea change developments globally and the Indian cement industry followed the international trend."

Recently, a low-carbon technology roadmap for the Indian cement industry has been launched in response to the sector’s need to cut its carbon footprint whilst meeting the growing demand for building materials in the country. It follows the launch of the global cement technology roadmap published in 2009. Enhancing energy efficiency and investing in newer technologies is one of the major objectives in the India-specific roadmap that aims to reduce the industry’s carbon emissions by 45 per cent by 2050. In an exclusive interview with Indian Cement Review, Philip Fonta, Managing Director, World Business Council for Sustainable Development says, "The Indian cement industry’s efforts to reduce its carbon footprint by adopting the best available technologies and environmental practices are reflected in the achievement of reducing total CO2 emissions to an industrial average of 0.719 tonne COf per tonne cement in 2010 from a substantially higher level of 1.12 tonne CO2 per tonne cement in 1996. The Indian roadmap outlines a low-carbon growth pathway for the Indian cement industry that could lead to carbon intensity reductions of 45 per cent by 2050. It proposes that these reductions could come from increased clinker substitution and alternative fuel use; further improvements to energy efficiency, and the development and widespread implementation of newer technologies."

Fonta further adds, "The vision laid out in the roadmap is ambitious but achievable. Wide stakeholder consultation took place throughout the process to bring in varied perspectives, and to reiterate that decisive action by all stakeholders is critical to realise the vision laid out in the roadmap. To achieve the proposed levels of efficiency improvements and emissions reduction, government and industry must join hands to take decisive and collaborative actions in creating an investment climate that will stimulate the scale-up of financing required."

"Energy efficiency index of Indian cement industries is better than the world average. This has been achieved by judicious selection of plant/equipments for greenfield projects/plant upgradation and adopting outstanding processes/practices. Installing latest equipments has resulted into incremental saving in terms of energy consumption, innovative efforts that lead towards quantum jump in terms of energy saving to be pursued," says Ratan K Shaw, Group Executive President & Chief Manufacturing Officer, UltraTech Cement Limited. He further adds, "Enhancement of blended cement share and fly ash/slag absorption will contribute not only towards energy reduction but will also help in reducing carbon footprint and thus paving the road to green solution."

According to him, the criteria for selection of equipment for new plants are as follows: input material properties viz. grindability, abrasiveness, moisture, presence of free silica, minor constituents, versatility in terms of grinding viz. OPC/PPC/Slag, output material properties-product fineness, PSD etc, investment and operating cost, scope for capacity enhancement and layout constraints in application of the technology. The operative norms desired are specific fuel and power consumption, environmental considerations, equipment reliability-easy to maintain equipment/proven performance.

The focus on energy efficiency for upcoming new plants as well as operating plants will contribute towards reduced energy demand and CO2 abatement, and he stresses on the selection of state-of-art energy efficient equipments /auxiliaries, latest automation systems/optimal systems/layout, integrated design with WHR power plants.

SN Subrahmanyan, Member of the Board and Sr. EVP, L&T Construction says, "The current focus is on savings in energy consumption and emission control methods, with stringent pollution control norms which are tightened day by day and the introduction of the PAT (Perform, Achieve and Trade) scheme. Cement manufacturers are expected to operate their plant in optimised conditions all the time. Power availability is also a key factor that affects cement plant operations. Clients are looking for equipment which reduces energy, fuel consumption, and effective utilisation of waste heat. Due to this trend, waste heat recovery systems and alternate fuel firing systems have become common requirements in cement plant tenders."

"Fuel efficient technologies have been adopted by majority of cement manufacturers," says Jayesh Somwanshi, Proprietor, Shreeyash Engineering. He adds, "A lot of affordable technology is now coming into the market. Also, there is a shift in focus of the manufacturers on the fuel efficient products which are really important for our industry."

Talking about the latest trends in technology, B Seenaiah, National President, Builder’s Association of India and Managing Director, BSCPL says, "The cement machinery manufacturers are obviously now focusing more on fuel efficient equipment. The manufacturers are now more keen on complying this latest emmission norm which helps save fuel and increases durability of the machinery." Explaining the same further, Martin Gierse, Managing Director, KHD Humboldt Wedag India Pvt Limited "We see that the trend is towards environmentally friendly and energy efficient products and services. As such, KHD has established themselves as one of the industry leaders in low NOx calcining technology, power efficient grinding technology and highly efficient pyro processing equipment requiring less heat and energy consumption, and thus avoids producing additional unnecessary CO2."

According to R Bhargava, Chief Climate & Sustainability Officer Shree Cement, periodic review of performance of various parameters of equipment with operating condition of plant at time of commissioning, year on year basis, checking of all parts of equipment at suppliers site, evaluation of energy efficiency for new equipment, determination of measuring points for evaluating the performance of plant are important factors while selecting plant and machinery with an approach towards energy reduction. Training on energy policy to vendors/contractors to design and construct energy efficient plant, efficient purchasing strategies, and incorporating specific energy consumption for every equipment in purchase order/contract etc, will also help moving towards the higher goal making an energy-efficient plant.

K Karunakara Rao, Dalmia Cement (Bharat) says, "The life cycle cost is a very important factor while selecting equipment. Deployment of higher capacity equipment bring added advantages of higher reliability, and easier supervision of operation apart from lowering overall cost per tonne, and will also reduce manpower. The higher capacity equipment also helps reduce the traffic on the haul roads, reduce the exposure of humans to the safety risk, and minimise the fugitive emissions. He also stressed the use of Vehicle Health Monitoring System (VHMS) that could help avoid unexpected machine downtime by a prognostic look at data changes over time, helps faster troubleshooting due to readily identified situations and causes. Another advantage is the in-advance arrangement for certified rebuilt parts for replacement, resulting in downtime reduction, which also helps achieve extended service life of the machine through proper operating method and maintenance work."

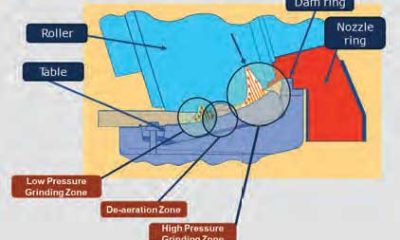

Highlighting the latest technologies in raw material grinding, Jayaraman says, "Selection of the type of grinding mill depends on the raw materials’ several physical characteristics, most important amongst them are hardness of the material and moisture content. Availability of the major grinding equipment in appropriate capacity decides complexity or otherwise of layout, auxiliary equipment sizing etc which ultimately decide the plant’s pyro-processing capacity. Vertical roller mills have been widely accepted for combined grinding and drying of moist raw materials in view of their excellent drying capacity and low energy consumption.

Although the principle of the vertical roller mill did not change over the years, many improvements have been made in design of the mill and other equipments in the grinding circuit resulting in less energy consumption and improved reliability. Introduction of external re-circulation of material, adjustable louvre ring and modification of mill body to improve the air and material trajectories are examples of such design changes." He further adds, "Apart from the main equipment viz. mill, classifier and fan, the efforts have been on improving the performance of internals e.g. table liners in case of vertical roller mills and classifying liners in case of ball mills. Use of mechanical conveying systems like bucket elevators are becoming more common in place of pneumatic conveying giving substantial savings in energy."

Market Trends

Gierse says, "The current situation is governed by the low utilisation of the cement production facilities on the one side and low speed in decision making and granting of permits on the other. This has made cement producers focus on reduction of operational cost and increasing efficiency. Some are working on optimisation of their product offerings to serve more specific needs of their respective clients. Only the very strategic players planned to expand their production base, following the good rule that makes you win market shares during low seasons. However, cement consumption grew in 2012 by 8 per cent, which is more than the GDP growth and proves the importance of this core sector."

However, KHD is not planning to launch any new equipment in the market but the focus remains on the further optimisation of, as well the systems for pyro and grinding sections with cost and performance. Talking about the requirements of the clients, Gierse said, "We do believe that our clients’ business cases can best be supported by offering services in achieving the maximum performance for their manufacturing plant."

Commenting on the situation, Gaurav Khanna, Managing Director, Ashoka Group says, "Currently the industry is going through a bad phase since the infrastructure projects are not happening and there is no business. However, we expect the industry to improve in the year 2014 due to elections otherwise to be honest; I do not expect much right now. The year 2013 will be similar to the previous year."

Somwanshi says, "Right now, our industry is not in a satisfactory phase. The projects have not been happening since a long time. Due to which, we are on the receiving end. Though, the announcement made by the government for the construction of 3,000 km road project has brought a huge relief, you actually do not know if they are implementing the same in six months time." Feeling the heat of slowness in the markets, Shreeyash Engineering, does not plan to launch any new equipment currently.

But Seenaiah was on a positive refrain. "I do agree that the cement equipment manufacturers are facing a tough time but by the end of the year, the cement companies will expand their capacity by 25 per cent, especially in the southern parts of India." He further adds, "The construction sector is divided into two parts, one is the building construction and the other is infrastructure projects. The building construction is picking up, but the infrastructure part is stagnant. The year 2013 will be marginal as the government is still taking a stock of the situation and change needs time." Manish Kumar, Head of Plant and Machinery, Supreme Infra, also supports the view. According to him, the industry is gradually coming back to the earlier pace. "I would say that the industry is going well, since there are projects that have been coming up which has reflected in the sale of equipment. We have recently purchased equipments, despite the government not doing enough for the industry."

The China Factor

Contributing nearly 15 per cent globally, Chinese equipment players have taken a significant share of Indian demand. But for some, the only advantage of the China brand is low price. Despite, the users combating several issues like bad quality and after sales services, the Chinese equipment continues to make inroads into the Indian markets.

"There are few plants in India which are running on equipment supplied by Chinese suppliers but the lifecycle of such plants are questionable. Some investors only see the initial cost of the project rather than the performance and efficiency of the plant. This trend is threatening the Indian suppliers who offer quality products at a moderate price. Dumping from China has affected not only the Indian market but industries globally. Most of the customers who purchased Chinese equipment for their plants are facing issues in operation as well as in maintenance areas like frequent breakdowns of core equipment, increased plant downtime and increased equipment replacement cost. This trend can only be arrested if our government takes concrete steps to curb dumping from China," says Subrahmanyan.

Seenaiah says, "The quality of machinery is cheap but it is fine for them, since their costs are low and ours are high. But the quality of our machinery is also much better as compared to theirs. For us quality matters and a lot of players have changed their preferences and have now shifted to Indian equipment."

Geirse begs to differ. He says, "I would not call this a threat. As western suppliers, the Chinese suppliers are today players in the global competition. The western suppliers have in the meantime opened up equivalent sourcing strategies to cater the clients’ need for the most favourable balance between technology and cost. India itself offers good opportunities for such sourcing, which lead to the fact that Chinese plant equipment manufacturers have yet to establish a significant presence in the Indian cement industry." Explaining the situation further, he said, "For India as an import destination, equipment manufactured in China loses its competitive edge when pitched against equipment manufactured domestically.

Duties, inadequate transport/handling infrastructure and freight costs are, possibly, the principal deterrents. In addition, the Engineering, Procurement and Construction (EPC) mode of project execution, at which the Chinese are particularly proficient, is yet to establish itself in the Indian context."

According to Somwanshi, the Chinese equipment cannot be labeled as æcheap quality ones’. Admitting the fact that a few players in the market have been known for its cheap price and substandard quality, he says, "Some companies are really good and their range of products are as competitive as ours. Now, that the Chinese manufacturers know that the customer opts for quality and not price, the companies have now been quality conscious and are adhering to the quality standards." But he quickly adds, "In fact, I suggest that our government should make policies that protect our economy from the Chinese."

Priority List

Voicing their concern over some of the major challenges Khanna, says, "Commencement of the projects which have been pending since long is the one thing that we would like to have. The other would be the reduction in import duty. Since long we have been demanding all this, but even during the budget the government didn’t announce any good policies. So we are stuck where we are and we are not able to move ahead."

According to Seenaiah, the projects worth Rs 40, 000 crore have been pending for a while which need to be cleared quickly.

He says, "The banking policies need to be in place since the companies are now cash-strapped to invest in any of these projects." Says Gierse, "On the policy level, government needs to push investment in infrastructure projects, and with regard to equipment and plant and machinery industry, the government should bring in similar kind of sops given during the 2009 budget, i.e reduction in excise duty for capital equipment. Further, if some changes could be done for abolition of entry tax, and implementation of GST, and bringing in uniform tax structure would lead to positive growth sentiments. According to Kumar, one of the biggest challenges for the industry today is the price rise. He also pointed out that the pending projects are worth crore of rupees resulting in cost escalation. He further adds, "The import duty has also been very high and even the budget hasn’t spelt out any reduction in the same." Valued at US$ 360 billion, India’s construction market accounted for five per cent of the US$ 7.2 trillion global construction market in 2010, and is expected to replace Japan as the third largest, after China and the US, by 2020.

As per India’s 12th Five-Year Plan (2012-17) document, the two segments most important to construction activity are infrastructure and housing. Since, infrastructure spending is expected to go up to nine per cent of gross domestic product (GDP) or US$ 1 trillion for the Plan period (2012-17), this will translate into double-digit growth for the demand of cement.