Concrete

Looking Beyond the Low Hanging Fruits

With the Net Zero targets looming in the near future and an imminent problem of emissions to contend with, the Indian cement manufacturing sector should no longer be satisfied with doing the bare minimum. Looking at innovative solutions, breakthrough technologies, automation and artificial intelligence, and most importantly, a change in mindset, is the need of the hour.

There is no denying the fact that cement being the second most consumed material after water in the world in terms of quantity, and by virtue of its inherent conversion process from limestone to clinker, the amount of CO2 emission from cement alone (7 per cent of all emissions) is one quarter of all industry emissions put together. Even in dollar terms the maximum CO2 per dollar of revenue industry-wide shows cement taking the top spot at 6.9 kg of CO2 per dollar.

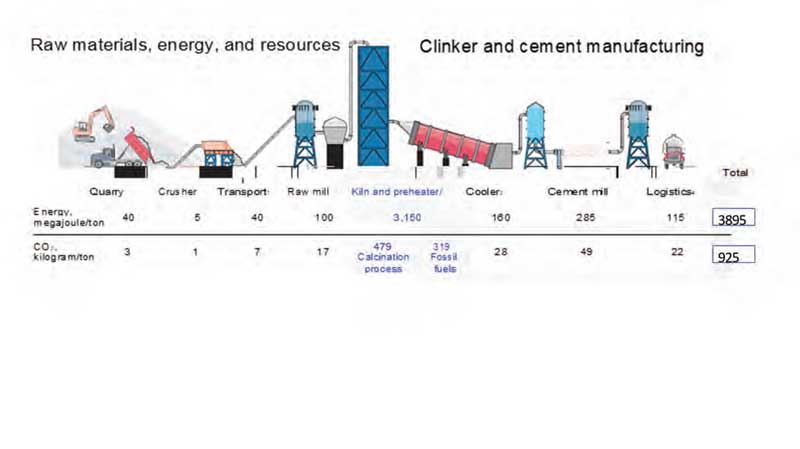

The process of cement making has majorly two areas – raw material resources and clinker and cement manufacturing, where the emission needs to be segregated into its constituent elements, both from the point of view of energy consumption and also in terms of CO2 emissions. While two-thirds of the emissions stem from the calcination process, which is where the bulk of the thermal energy is consumed, the raw material extraction to feed generates negligible amounts of emissions and the cement grinding from clinker and logistics makes the bulk of the remaining emissions. The total emissions of 925 kg per tonne of cement production leaves a staggering 4 billion tonnes of CO2 generation each year, as the world produces 4.2 billion tonnes of cement annually.

The pathways through which the industry has progressed so far can be seen in the following areas:

- Energy Efficiency

- Alternative Fuel

- Clinker Substitutes

- New Technologies

- Alternative Building Materials

If one goes into the analysis of each of these levers that the cement industry is currently using, the first three have remained the low hanging fruits where most of the attention and energy had been diverted to. These top three levers have so far fetched about 25 per cent of the CO2 emission reduction possibility into 2050, with energy efficiency showing a possibility of 7.2 per cent, alternative fuel a possibility of 10.5 per cent and clinker substitution 7 per cent. However, the investments needed for these and the abatement cost per tonne of CO2 would look very different for each. For example, alternative fuel would still need disposal cost, carbon capture and storage as well and the investments for these would make this category the highest in terms of abatement cost. The following table gives this as follows among all the levers:

So far, the cement industry has focused on the low hanging fruits, mostly clinker substitution after working on efficiency improvement levers, where the abatement costs were negative, giving economic benefits to the cement makers. Driven by the country’s landfill laws and pollution control norms, some of the advanced countries have outright rejected use of coal and PetCoke in cement kilns, replacing that with alternative fuel and biomass. However, these have to go through the abatement cost of Carbon Capture and Storage, which has been so far very high. Let us go through each category and see what is the current stage of development of these areas of focus.

Efficiency Improvement: The last step change for cement kiln technology was in the case of dry process replacing the wet process, thereafter the recent advancement has happened in the use of electrical energy instead of thermal energy for the kiln conversion process. This has been put to commercial use but till we use renewable energy in kilns, this does not give any advantage in terms of overall gain in emission. The replacement cost of thermal to electrical could be very high as well, so the future electrification of kilns, depends on use of renewables that must be part of a stable grid power, which raises many actions to be taken.

Clinker Substitution: Maximum gains have happened so far in reduction of emission by adopting various means to replace clinker with fly ash, slag etc., but the future could actually have very little of this available as generation of electricity moves to the renewable mode and the steel companies adopt more of the green technology that would generate far less waste eventually from the process.

Alternative Fuel: The availability of alternative fuels depends largely on the development of local supply chains that must wade through a number of constituencies like the local municipalities for the municipal wastes and the development of logistics systems have a lot to be desired. The only hope remains the use of biomass, which is the highest growing segment. The investments here include not only the platforms but also avenues of de-chlorination, etc.

Carbon Capture Use and Storage (CCUS): This method isolates and collects CO2 from industrial emissions and either recycles it for further industrial use or safely stores it underground. Once captured, a wide variety of potential uses for CO2 could be possible, such as in the production of glass, plastics, or synthetic fuels. Though carbon-capture technologies do exist commercially, they are utilised in very few plants—one example being natural-gas plants. Therefore, the progress of extensive decarbonisation will not only depend on the economic viability of storing and sequestering the carbon but also on the availability of CO2 marketplaces, through which the captured CO2 can be sold.

Carbon-cured Cement: This technology injects CO2 captured during cement production to accelerate the curing process and ‘lock in’ CO2 in the end product. Current low-carbon cement technologies can sequester up to 5 per cent of CO2, with the potential of 30 per cent. In fact, 60 million tonnes of CO2 per year are projected to be stored via carbon-cured concrete in 2050.

Alternative Building Materials: In the years to come, alternative building materials could shift demand away from cement. To date, cross-laminated timber (CLT) has attracted the most attention. Made by gluing wooden panels and boards together, CLT is an adequately fire-resistant building material that can reach large dimensions. Its application has recently increased and includes projects in Canada, Japan, and Sweden. Assuming a 10 per cent replacement of concrete—and considering the CO2 captured in the wood has been abated—would reduce the overall cement footprint by 25 per cent, as even more

CO2 is captured than avoided by reducing the cement production.

Recycled Concrete: Use of recycled concrete and demolition waste is the new development especially in Europe with the sources of limestone becoming limited in the future.

The potential reduction of 50 per cent of the CO2 emissions by 2050 depends on the progress of carbon capture and storage systems and technologies, where we have a few start-ups who have come up with very different processes. For example, one start-up uses a lower proportion of limestone in its cement, which results in fewer process and fuel emissions; this company’s process also locks in additional CO2, which is added before the concrete cures. Adding CO2 makes the concrete stronger and reduces the amount of cement needed. Carbon-cured concrete could also use CO2 captured during cement production. Today’s methods could sequester up to 5 per cent of the CO2 produced during production, but newer technologies could sequester 25 to 30 per cent. Products such as carbon-cured concrete, positioned differently, could earn a ‘green premium,’ potentially giving companies an edge among environmentally conscious buyers and greater pricing power.

The Indian cement industry must move steadily to these new innovations, after making the maximum gains from the low hanging fruits. Innovation remains the key word and investments in innovation, including the mindset, for cement is the first step in this journey.

-Procyon Mukherjee